")

Beyond Future Energy Scenarios: How significant is the challenge of 12 million EVs by 2030?

National Grid’s Future Energy Scenarios Consumer Transformation pathway estimates that we’ll need 12 million battery electric (BEV) on the road by 2030 to meet our net zero targets. This is a significant number of BEVs but is it achievable?

What are the Future Energy Scenarios (FES)?

FES are broad and in-depth frameworks that many organisations use to help understand trends, trajectories, and track progress towards a net zero UK. They are compiled through a great deal of research, as analysts try to predict the future through a great many uncertainties.

FES has 4 comprehensive and holistic pathways to net zero that considers the short, medium, and long-term factors in energy supply and demand. These pathways are:

- Falling short – The slowest pathway that predicts minimal behavioural change and only the decarbonisation of power and transport by 2050.

- Consumer Transformation – Heating is electrified, consumers will change their behaviour, there’ll be high energy efficiency, and demand side flexibility by 2050.

- System Transformation – Hydrogen is used for heating, consumers won’t change behaviours quickly, lower energy efficiency, and supply side flexibility by 2050.

- Leading the way – The fastest pathway that predicts significant lifestyle changes, and a mixture of hydrogen and electrification for heating by 2050.

Across all these scenarios the transportation system is a key focus. In our work with local authorities, most of them have used the FES Consumer Transformation (FES CT) pathway to support their EV infrastructure planning. Distribution Network Operators (DNOs) use FES as the starting point for a number of more detailed models, including their Distributed Future Energy Scenarios. Whereas Charge Point Operators (CPOs) have used FES to understand the future market demand.

")

What does FES CT say about electric car adoption?

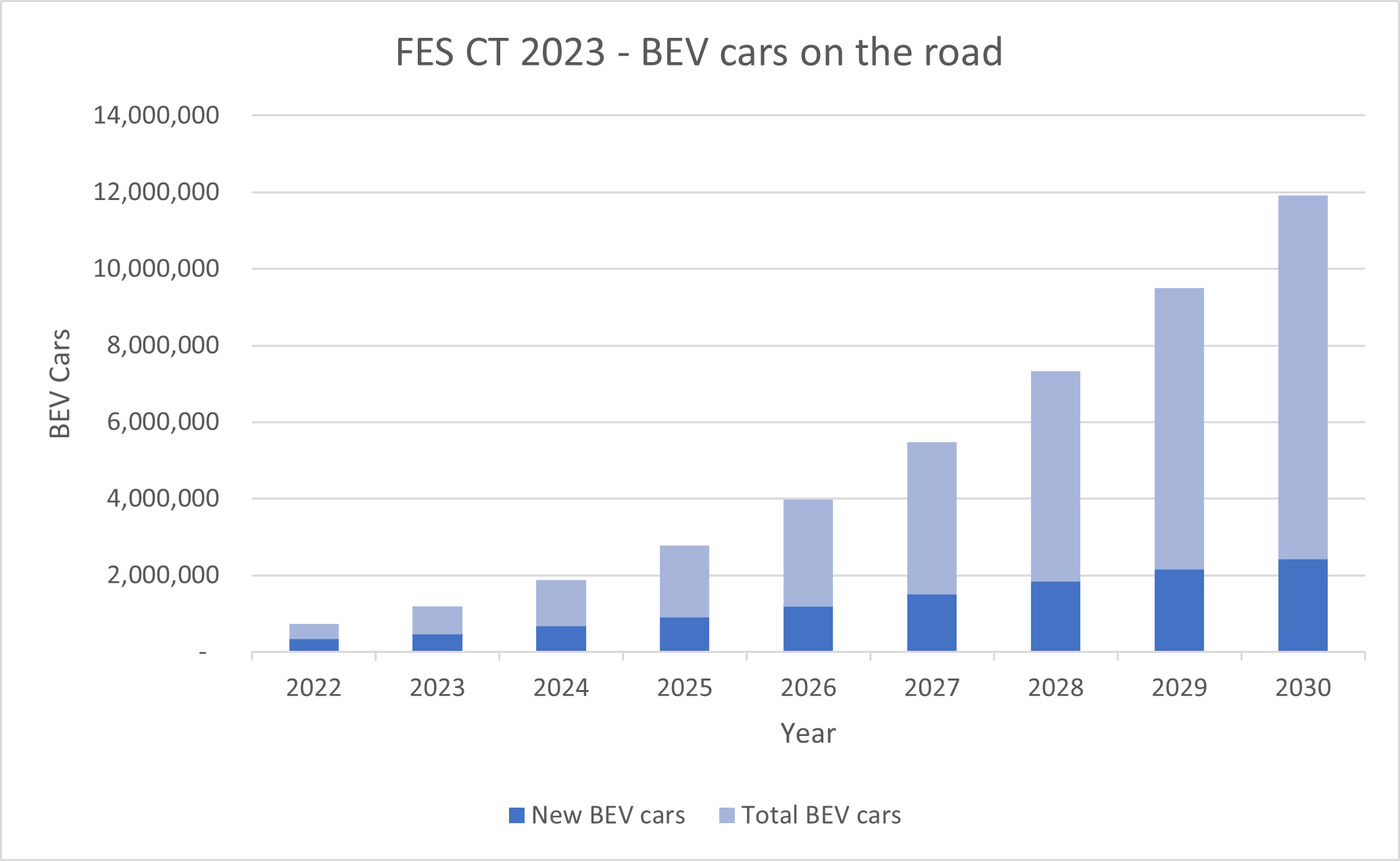

FES CT predicts there will be just under 12 million BEV cars on the road by 2030. This suggests that BEV numbers are going to rise at very fast rates with significant annual increases.

EC.11: Battery electric cars on the road for 2023

FES CT predicts there’ll be 470,843 new battery electric cars sold this year – this will continue to grow year-on-year. In 2030, 2.4 million new electric cars will need to be sold if the forecast is to remain on track.

")

How significant is this challenge?

It’s perhaps a greater challenge than most people understand. In order to hit the 2030 number, the market will have to see an unprecedented increase in the market share of one vehicle type.

Last year (2022), 1.6 million cars were sold, with 267,203 of those being BEV (73,715 fewer than FES CT predicted). This year, the whole new car market has grown by 18%, factoring in this growth, we’ll probably sell around 1.9 million new cars in 2023 – 25% (470,843) of these will need to be BEVs to reach the FES target. To put that into perspective Toyota, Volkswagen, Ford, and BMW collectively only sold 470,000 new cars in 2022.

To keep on track in , 34% of new car sales will need to be BEVs. Assuming total sales of 2 million new cars, this means 678,566 BEVs. That would be the equivalent of all the cars sold by Toyota, Volkswagen, Ford, BMW, Mercedes-Benz, Peugeot, and Nissan in 2022.

")

What challenges are in our way?

BEV adoption is affected by so many factors including infrastructure development, government policies and incentives, consumer preferences, and economic conditions. Some factors will speed up or slow down adoption, and some will limit its total speed – one of these is supply – how many BEVs that will actually be available to buy.

From a global markets’ perspective, we need to think internationally and about other countries striving to achieve similar goals in similar timescales. As more nations prioritise the transition to electric vehicles, the demand for batteries and other essential components will increase, and domestic needs will be prioritised.

Just looking at battery production, the UK has a 1.7GWh AESC battery plant in Sunderland, which the government will reportedly invest in to increase capacity to 9GWh by mid-decade. The larger plant would create enough batteries for 100,000 cars each year (remember we need 678,566 BEVs in 2024) The recently announced Tata Group gigafactory in Bridgewater will produce 40 GWh worth of when it opens in 2026. That’s the equivalent of 533,333 Tesla Model Y batteries (based on Model Y battery capacity of 75kWh) or 1 million Nissan Leaf batteries (based on a Nissan Leaf battery capacity of 40kWh). So domestic support for our BEV requirements looks incomplete.

China has over 100 operational gigafactories so with their additional capacity they could supply enough volume of BEVs. However, China would need to want to supply us rather than other countries, and we would need the political will to ask for that support.

A significant but not impossible challenge

Reaching the physical distribution of 12 million BEV cars by 2030 will be a monumental challenge. We will have to consistently sell more vehicles than we have ever sold before and we’re already behind. It is achievable but only with increased efforts from across government, industry, and consumers.

A significant challenge, yes! An impossible one, maybe not.